Welcome to the ADVISORY PORTFOLIO MANAGEMENT (apm) AUTUMN 2023 Quarterly Review.

The Advisory Portfolio Management (APM) Quarterly Review provides clients within the service a review of the financial world over the last three months, and how this may have affected their pension or investment. If you would like to read more about this service, please Click Here.

A key part of the reporting is the colour coding. Each APM portfolio is colour coded to enable you to spot which category applies to you. The relevant information is then presented in a clear and easy to understand way. However, if you require any further clarification, please do not hesitate to get in touch.

MARKET OVERVIEW - QUARTER THREE 2023

The third quarter began in the same vein as the second ended, with markets believing that falling inflation supported the belief that the interest rate cycle had or was very close to peaking. Furthermore, the so-called goldilocks scenario which would see growth remain positive and central banks cut rates sooner in 2024 than was originally being indicated. As we progressed further through the quarter however, the narrative began to change with oil prices increasing sharply as Russia and Saudia Arabia cut production, pushing up bond yields which in turn led markets to wake up to the possibility of rates being higher for longer.

As we turn our attention to the final quarter of the year the focus is likely to remain on two key factors. Firstly, how inflation behaves will be crucial to investor sentiment. If we see inflation falling more quickly, optimism will build that interest rates have definitively peaked and in turn can fall faster. Stickier inflation however switches back to a higher for longer message. Secondly, will be the resilience of growth in the key markets of the US, China and Europe, should data support the belief that we can avoid a recession it will help investors look through the short term, to sunnier times ahead. Deteriorating data however, could sour the mood and lead to the conviction that interest rates have been pushed too high, causing a sharper downturn or hard landing.

Beyond the end of 2023, the focus may shift to company earnings, which ultimately tends to drive the direction in markets over the medium term. The picture however is more confused as some areas, such as UK equities, property and bonds which look cheap, whilst others look much more fully valued. It may well prove that we are entering a period where single themes no longer drive outperformance and a more balanced and diversified approach works best.

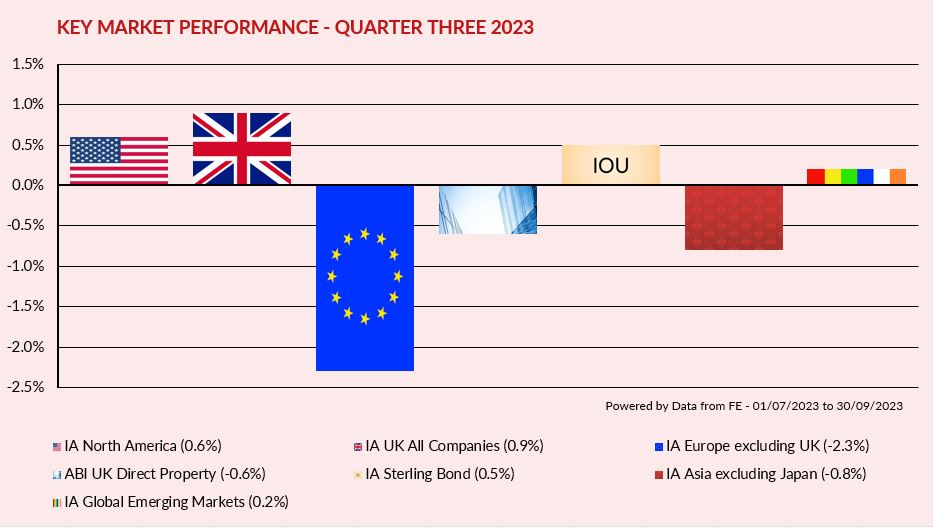

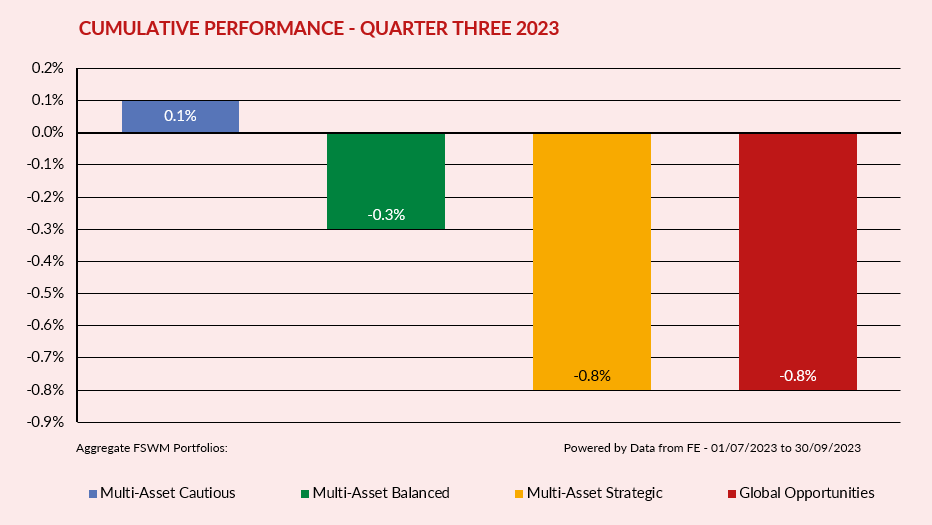

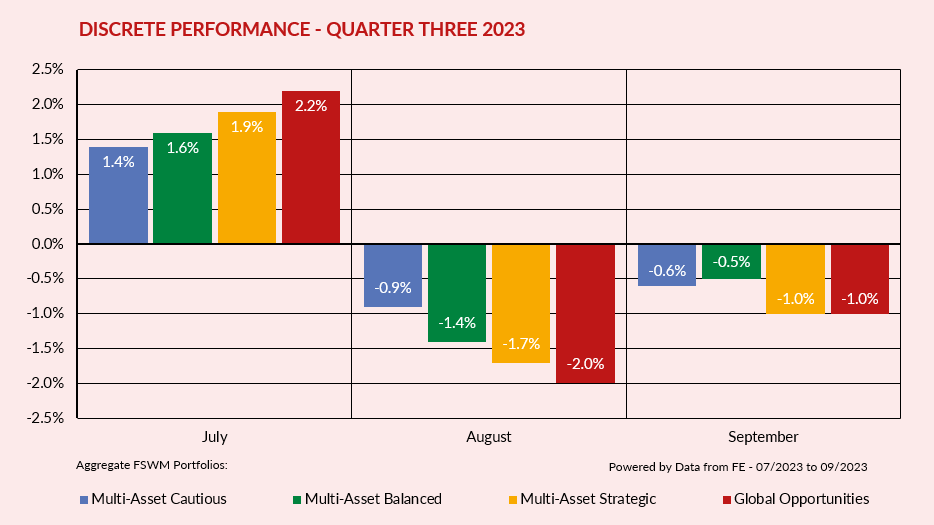

APM PORTFOLIOS - QUARTER THREE 2023 PERFORMANCE

The graphs below show how the APM portfolios within the four Finance Shop risk categories have behaved over the last three months. The first graph shows the total return for the quarter whereas the second graph illustrates the “month by month” performance. The performance figures are aggregated so, for example, the green bar is made up of all the APM Multi-Asset Balanced portfolios across all product types.

If you require specific performance figures for your plan, please contact your adviser.

PERFORMANCE REVIEW

Portfolios were dragged backwards over the second half of the period and all but our cautious portfolio posted negative returns. Falls however were modest and a weaker Sterling helped offset some of the impact.

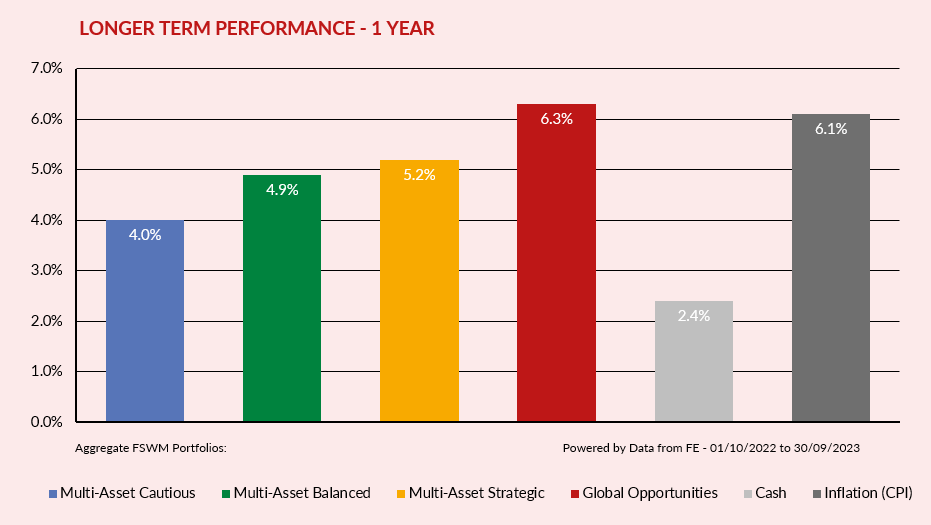

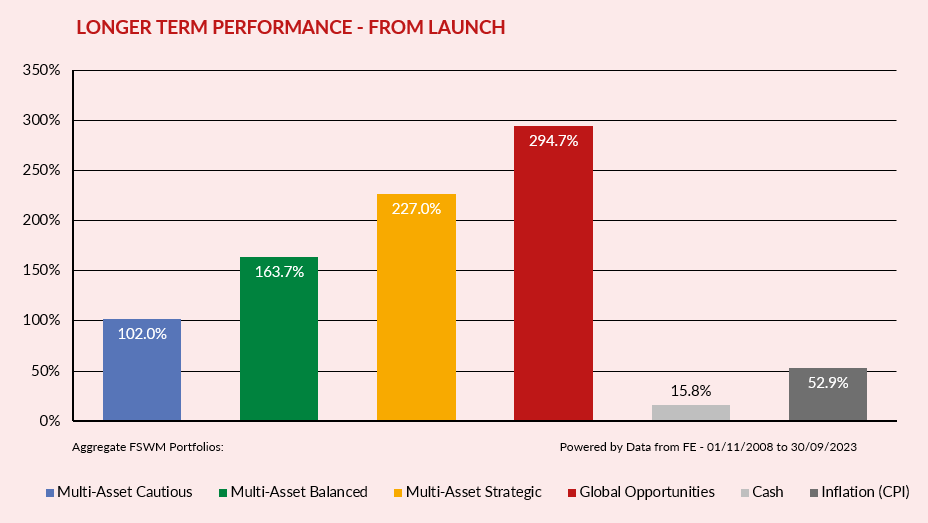

APM PORTFOLIOS - LONGER TERM PERFORMANCE

The first graph below shows how the APM portfolios have performed over 12 months. For comparison, the returns of cash (MoneyFacts 90 days’ notice 10K) and inflation (UK Consumer Price Index) are also shown. The second graph illustrates how the portfolios have performed since launch (1st November 2008).

As with the Cumulative & Discrete Performance graphs, the figures for each category are aggregated.

APM FUND REVIEW POLICY

A key part of the APM service is to monitor the underlying performance of each fund within the portfolios for both risk and return. We have selected quality funds with strong track records and therefore do not envisage a high turnover of holdings.

However, there will be occasions when the performance of an individual fund will lead to its expulsion from the portfolio(s). There are several factors that determine this decision, for example consistent under-performance, change of management team etc. It is also important, however, to have patience with a fund that is just suffering short-term under-performance.

We operate a “traffic light” system and will move a fund from a “green” to “amber” rating if the fund requires closer scrutiny at the next review. If a fund shows sufficient improvement, it will move back to “green”.

If the fund consistently under-performs without good reason its status will change to “red” and the fund will be removed from the portfolio(s). A replacement fund will be selected and all clients holding the fund within their portfolio will be notified. Upon receipt of their authority, the client’s funds will be switched accordingly.

RESULTS OF FUND & ASSET ALLOCATION REVIEW

The Investment Committee meets on a quarterly basis and one of its primary functions is to review our existing fund range.

Within this meeting we scrutinise any funds which we feel are performing significantly differently to their peer group or benchmark, with a number then run against our internal performance and risk measurements.

The funds under review are as follows:

- Aberdeen Europe

- Brooks Macdonald Defensive Capital

- CT American Select

- TM Crux UK Core

- Downing Unique Opportunities

- Fidelity Strategic Bond

- Gravis UK Listed Property

- Gravis Digital Infrastructure

- JPM Emerging Markets Growth

- Jupiter Monthly Alternative Income

IMPORTANT INFORMATION

This report has been issued by the Investment Committee of the Finance Shop Wealth Management team using data provided by Financial Express. Care has been taken to ensure that the information is correct but Financial Express and Finance Shop neither warrants, represents nor guarantees the contents of the information, nor does Financial Express or Finance Shop accept any responsibility for errors, inaccuracies, omissions, or any inconsistencies herein.

Past performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amount originally invested. Currency fluctuations can also affect fund values. The above report does not constitute advice and you should speak to your Independent Financial Adviser before you make any alterations to investments or pension plans.

The instruments recorded above are weighted model portfolios created using Financial Express Analytics. Performance figures shown are based on the weighted models and may differ from the actual returns achieved by investors. Performance figures shown are based on bid-to-bid gross returns and do not include plan, contract, or ongoing adviser charges / commission. Please refer to your policy documentation for further details.